'%3e%3cpath%20d='M35.0714%200.646484L25.1609%2010.5367L69.9475%2035.498L35.0714%200.646484ZM69.9475%2035.498L25.164%2060.4613L35.0714%2070.3487L69.9475%2035.498ZM25.1606%2010.537L0.149414%2035.4969L25.1606%2060.4579V10.537Z'%20fill='url(%23paint0_linear_2133_2410)'%20fill-opacity='0.980392'/%3e%3cpath%20d='M69.9492%2035.4995L25.1621%2060.4646V10.5381L69.9492%2035.4995Z'%20fill='white'%20fill-opacity='0.980392'/%3e%3cpath%20d='M132.506%2045.6554V49.1118H111.132V21.8818H132.473V25.4226H115.184V33.3471H132.49V36.8035H115.184V45.6554H132.506Z'%20fill='white'/%3e%3cpath%20d='M142.621%2021.8818V45.6554H159.168V49.1118H138.569V21.8818H142.621Z'%20fill='white'/%3e%3cpath%20d='M153.848%2021.8818H178.498V25.4226H168.199V49.1118H164.147V25.4226H153.848V21.8818Z'%20fill='white'/%3e%3cpath%20d='M186.266%2021.8818H182.214V49.1118H186.266V21.8818Z'%20fill='white'/%3e%3cpath%20d='M211.506%2049.1118L203.233%2038.1524L195.045%2049.1118H189.979L200.785%2035.2018L190.486%2021.8818H195.72L203.487%2032.4198L211.506%2021.8818H216.487L206.019%2035.2018L216.825%2049.1118H211.506Z'%20fill='white'/%3e%3cpath%20d='M81.8389%2021.8818H95.6836C103.872%2021.8818%20107.587%2027.1929%20107.587%2035.1175C107.587%2042.7048%20104.294%2049.1118%2095.9369%2049.1118H81.8389V21.8818ZM95.7681%2045.6554C102.437%2045.6554%20103.619%2040.0914%20103.619%2035.2018C103.619%2030.3965%20102.015%2025.4226%2095.0082%2025.4226H85.891V45.6554H95.7681Z'%20fill='white'/%3e%3c/g%3e%3cdefs%3e%3clinearGradient%20id='paint0_linear_2133_2410'%20x1='0.000308559'%20y1='35.4976'%20x2='70.1843'%20y2='35.4976'%20gradientUnits='userSpaceOnUse'%3e%3cstop%20stop-color='%2300B8FF'/%3e%3cstop%20offset='1'%20stop-color='%233C63AD'/%3e%3c/linearGradient%3e%3cclipPath%20id='clip0_2133_2410'%3e%3crect%20width='220'%20height='70'%20fill='white'%20transform='translate(0%200.5)'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Ember

Advanced Order Management

and Execution Platform

Backed by nearly 20 years in trading tech, Ember is our fastest, most advanced platform yet.

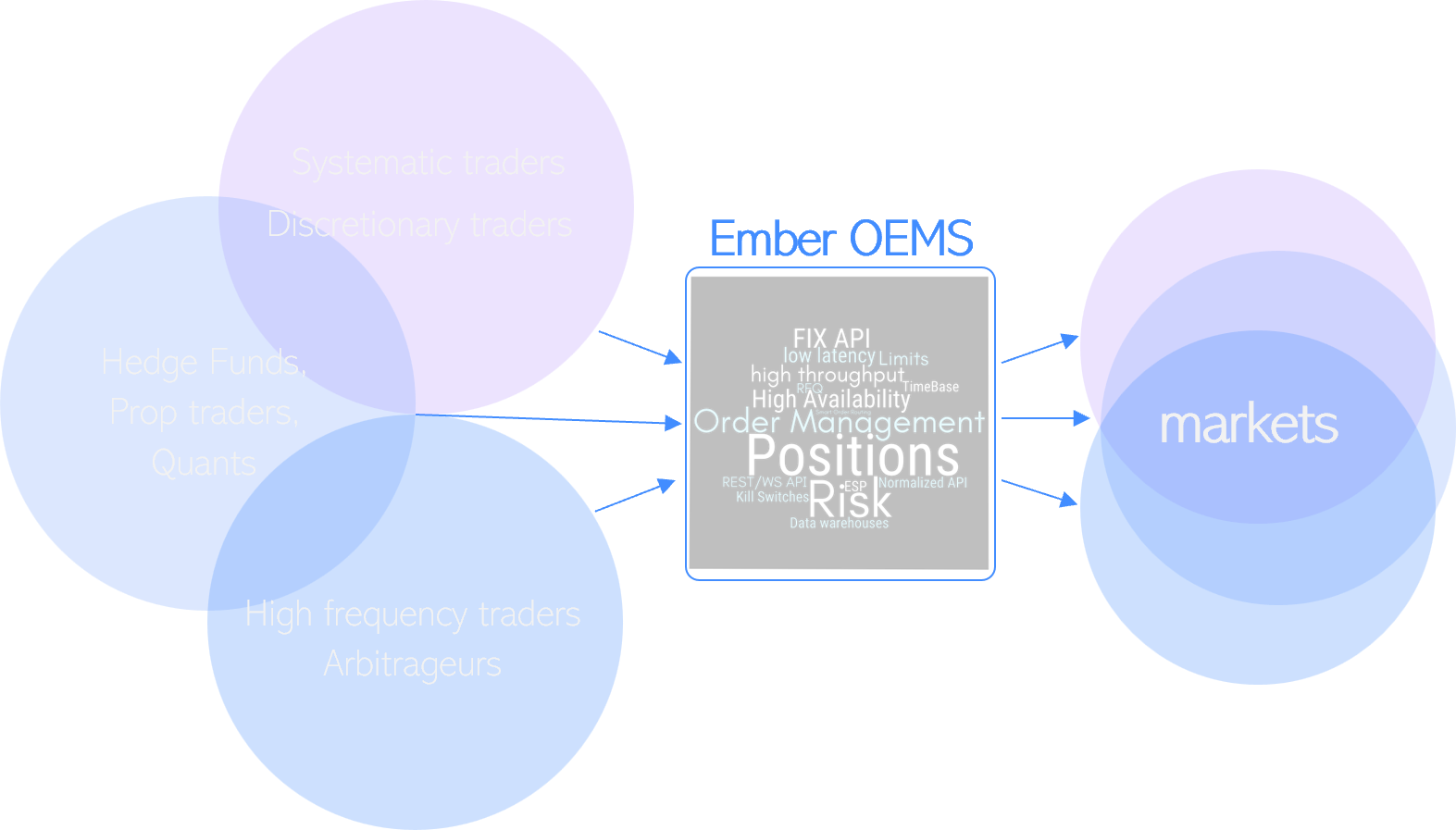

You can use Ember for

OEMS (Trade Hub)

Ember’s Trade Hub serves as a unified, normalized API gateway to diverse markets across most asset classes — ranging from exchange-traded synthetics to cryptos. Trade Hub offers extensive API support with FIX 4.4 / 5.0 and REST / WebSocket gateways, complete with Java, Python, and JavaScript sample code to simplify integrations.

Trade Hub’s order-entry capabilities include robust Risk controls, configurable Kill Switches, multi-projection Position tracking. It supports SMART order routing and provides out-of-the-box execution algorithms like TWAP, VWAP, PVOL, and ICEBERG. For this use case Ember provides Java SDK to develop custom execution algorithms and implement functionality like internal order crossing based on customer specs. Trade Hub supports Executable Streaming Prices (ESP) with Market-by-Price and Market-by-Order depth and Request for Quote (RFQ/RFS) workflows. It provides advanced Market Simulation capabilities that enable back testing and real time paper trading.

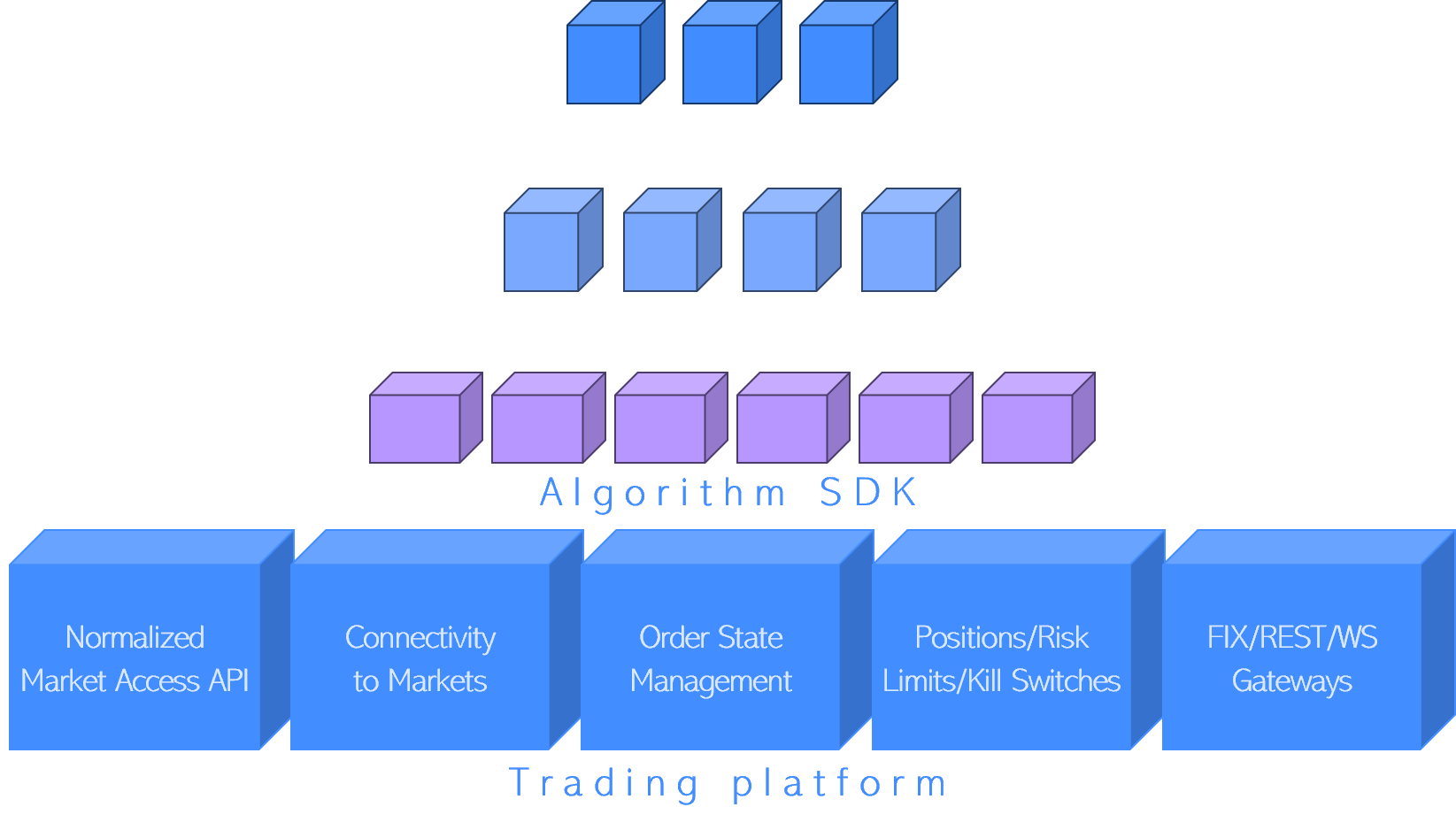

Trading Algorithms

Ember provides a Java SDK for building custom execution co-lo algorithms. Its normalized APIs for market data venues, order book interactions, and order entry offer a reliable abstraction layer. Combined with market simulators and the ability to debug code directly in IntelliJ IDEA, Ember significantly reduces time to market.

Cross-connected Ember instances can be deployed in different data centers around the world, enabling various market-making and arbitrage strategies.

Ember includes a set of standard algorithms, such as smart ICEBERG, market-chasing TWAP, VWAP, and Participation Volume (PVOL), all built using the Algo SDK.

Additionally, Ember provides FIX and REST WebSocket APIs for implementing trading logic externally in Python, Java, JavaScript, and other languages.

Custom Dark Pools / Matching Engines

Ember can be used to implement low-latency matching engines, with matching logic programmed using Ember's Algorithm SDK (Java). The following types of solutions have been successfully built:

- Central Limit Order Book (CLOB) matching engines (a CLOB sample is included in the SDK).

- Internally crossing matching engines that maintain passive orders in the book and route aggressive orders to external venues when opportunities arise.

- Matching engines with RFQ capabilities.

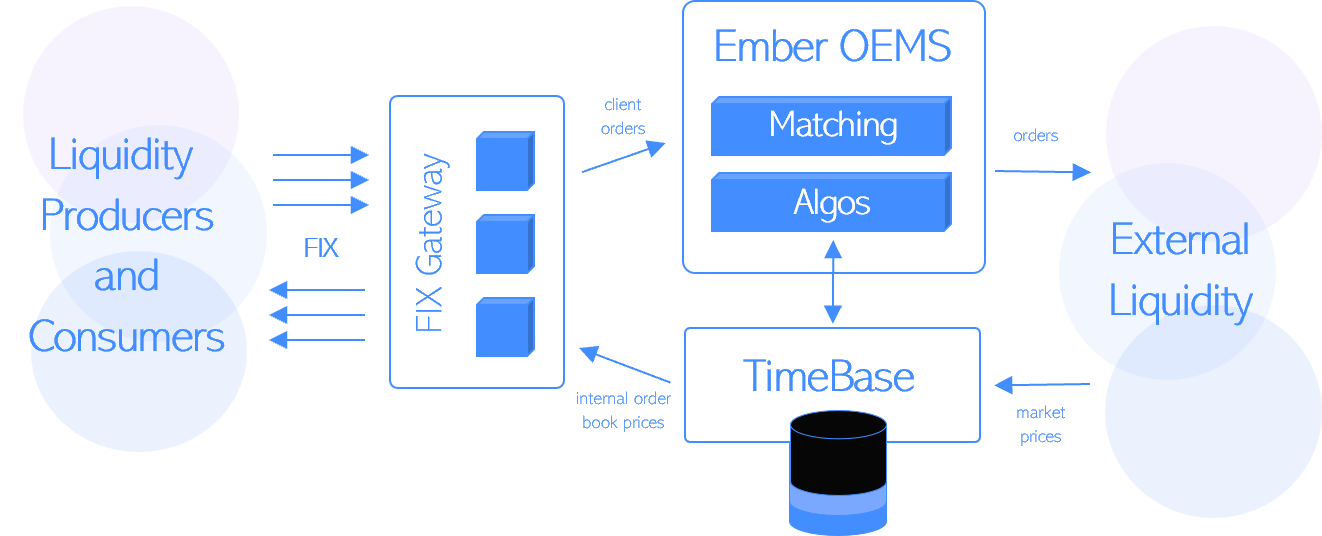

Matching engines typically publish Market-By-Order price feeds to TimeBase. Ember can then rebroadcast these feeds via the FIX Market Data Gateway to matching engine participants. With Ember's optimized architecture, the end-to-end latency for order-to-fill operations can be as low as 5-6 microseconds, measured at the OS network layer.

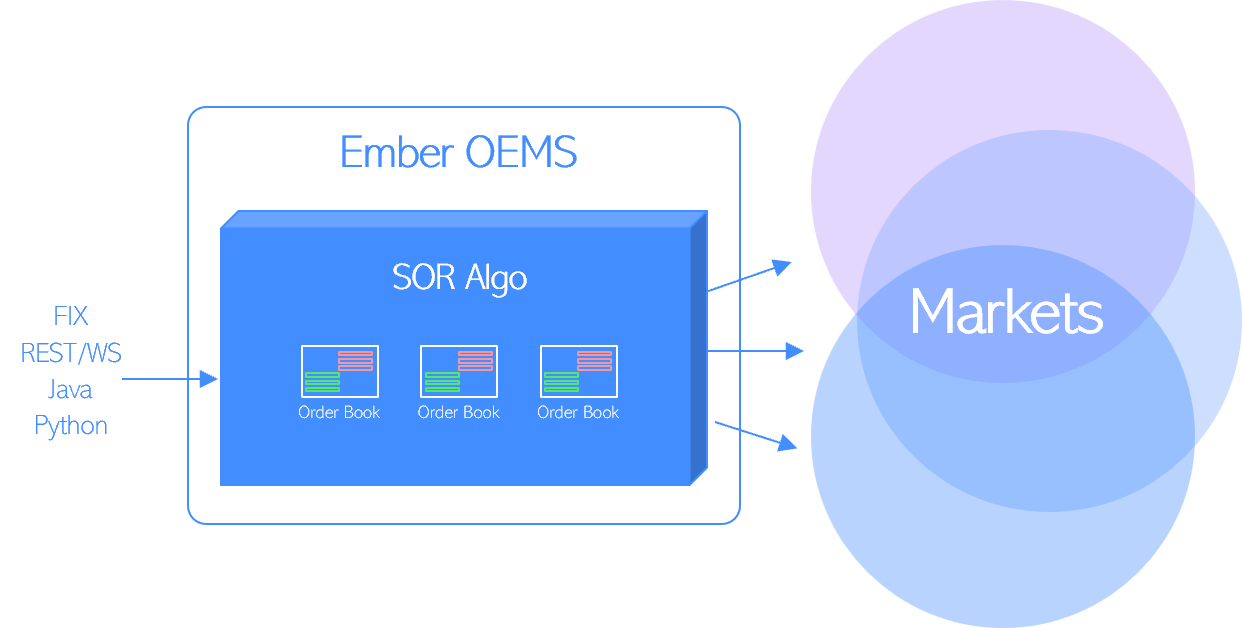

Smart Order Routing (SOR)

Ember includes a standard Smart Order Routing (SOR) algorithm designed to optimize execution across multiple exchanges. For a given order quantity, the SOR algorithm constructs an execution plan by evaluating the following factors for each exchange:

- Available liquidity, starting from the top of the book

- Commissions charged by the exchange (e.g., maker/taker fees, trade volume discounts)

- Available account balance on the exchange

- Recent rejection statistics for the exchange

- Per-exchange security metadata, including order price precision, quantity precision, minimum order size, and more

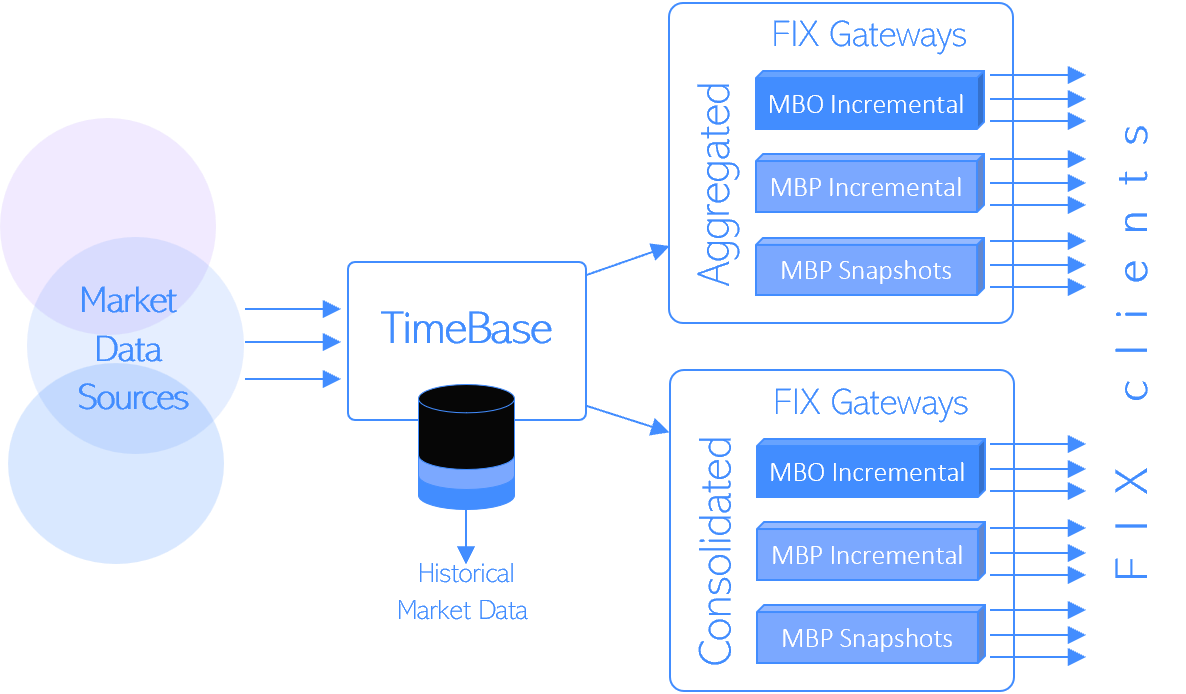

FIX Market Data Gateway

When combined with TimeBase, Ember can be used to redistribute market data to numerous FIX clients (commonly referred to as "FIX Fan-out"). Market data can be ingested into TimeBase from a variety of markets and protocols, ranging from ITCH and MDP to WebSocket, and then redistributed to interested parties in a normalized FIX format.

Depending on the specific needs of different client groups, Ember can distribute aggregated and consolidated order books, broadcast Market by Order (Level 3) and Market by Price (Level 2) feeds with configurable depth (limited or unlimited) and throttling. Its highly efficient FIX engine and gateway design enable feeding data to hundreds of clients seamlessly.

Ember integrated with the 150+ market venues:

Your venue not in the list? We have a dedicated team who specialize in market integrations

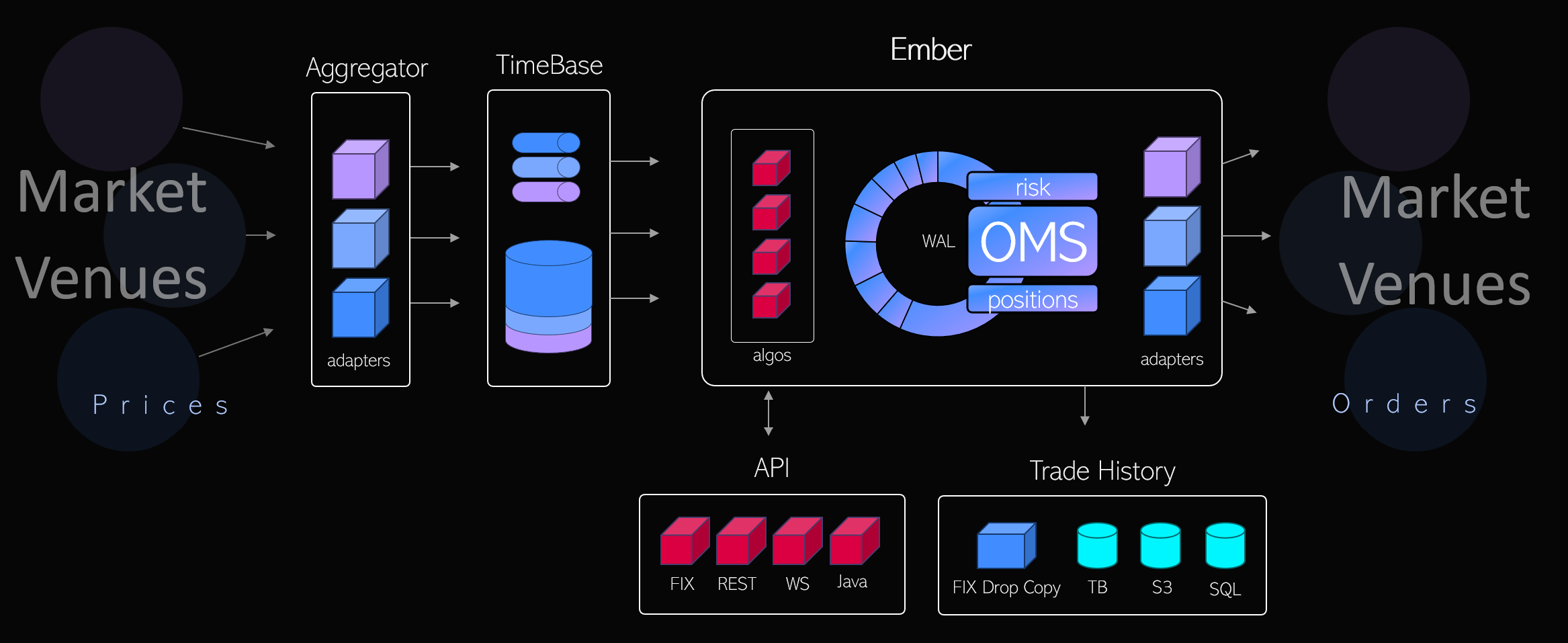

- Market Data Aggregator: A service that normalizes and aggregates market data from various sources, storing it in TimeBase.

- TimeBase: A time-series database developed by Deltix, used for market data aggregation, distribution, and custom complex event processing. For low-latency market data consumers (such as certain Ember algorithms), TimeBase offers IPC/Unicast topic channels that deliver nearly 100x the throughput and latency improvements over traditional data streams..

- Ember: The core service that manages Order and Position State, performs pre-trade risk checks, and runs algorithms with custom trading logic and adapters for each target trading venue. Ember uses an event-sourcing architecture and features a Write-Ahead Log (WAL or Ember Journal) to record trading requests and events impacting the OMS state. In high availability mode, the journal is synchronously replicated from the leader to the follower Ember instance. On-the-fly journal compaction and trading history warehousing support 24/7 system operation under heavy load.

- Trade History: Trading history can be streamed to various data warehouses for long-term storage and integration with back-office pipelines. This approach follows the CQRS design pattern, offloading intensive data queries from the OMS. Supported data warehouses include TimeBase, ClickHouse, Kafka, S3/Athena, Amazon Redshift, and RDS SQL Server. Ember also offers FIX Drop Copy services and distributes daily trading reports via mailing lists.

- APIs: Ember includes high performance FIX Gateways capable of servicing hundreds of Market data and Order Entry clients. REST and WebSocket gateway simplifies Python/JavaScript client integrations. Ember includes high-performance FIX gateways capable of serving hundreds of market data and order entry clients. The REST and WebSocket gateways facilitate Python and JavaScript client integrations. Ember also provides a Java RPC API that offers optimal performance for external order entry and enables remote control of Ember's internal operations.

-

Our address:

US Headquarters: 21 Drydock Avenue, Suite 410 W, Boston, MA 02210 -

Phone numbers:

Toll Free: +1 800 856 6120

Phone: +1 617 273 2540

Fax: +1 781 207 1296

-

E-mail:

Global Sales enquiries: sales@deltixlab.com

Media/Press enquiries: press@deltixlab.com

-

Press / media:

For media and press inquires, contact us at +1 800 856 6120 or press@deltixlab.com